Scrit Patel

Scrit Patel

Pulin Sheth

Pulin Sheth

Shweta Khera

Shweta Khera

Jaydeep modi

Jaydeep modi

Hitesh Malviya

Hitesh Malviya

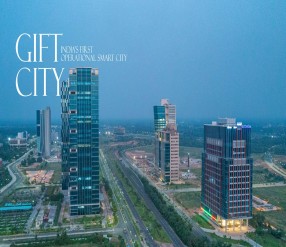

How gift city play major role in asian economy and finance

The significance of GIFT City (Gujarat International Finance Tec-City) in the context of the Indian...

Why Choose GIFT City Gandhinagar Gujarat for Investment

Best opportunities to invest in gift city Gandhinagar in commercial and residential schemes. Strateg...

Investment opportunities in GIFT CITY | Global Business Epicentre

Global investment opportunities in GIFT City “The vision for GIFT City is to create a World...

History and tax incentives of GIFT City

In 2008, the then-Gujarat Chief Minister Mr. Modi initially revealed that the state government would...

Right time to invest in Real-estate at GIFT City

In 2008, the then-Gujarat Chief Minister Mr. Modi initially revealed that the state government would...

Gujarat’s largest mall to come up in Thaltej

Gujarat’s largest mall will come up on S G Highway, at Zydus Hospital Crossroads. Ph...